what is credit card and how to use it

A credit card is a financial tool that allows you to borrow money from a financial institution, typically a bank, up to a certain predetermined limit, to make purchases or pay for services. It’s essentially a form of short-term, unsecured debt. Here’s how it works and how to use it responsibly:

1. Applying for a Credit Card:

- You apply for a credit card with a bank or credit card issuer. They will review your credit history, income, and other factors to determine whether to approve your application and what credit limit to offer.

2. Understanding the Key Terms:

- Credit Limit: This is the maximum amount of money you can borrow on your card.

- Interest Rate (APR): The annual percentage rate represents the cost of borrowing money if you carry a balance from month to month. It’s expressed as a percentage.

- Minimum Payment: This is the smallest amount you must pay each month, typically a percentage of your outstanding balance.

- Grace Period: Many credit cards offer a grace period, during which you can avoid paying interest if you pay your balance in full by the due date.

3. Making Purchases:

- Once approved, you can use your credit card to make purchases in stores, online, or over the phone. The card issuer pays the merchant, and you owe the card issuer the amount spent.

4. Monthly Statements:

- The credit card company will send you a monthly statement detailing your transactions, the minimum payment due, the due date, and the total balance.

5. Paying the Bill:

- It’s crucial to pay at least the minimum payment by the due date to avoid late fees and a negative impact on your credit score.

- Paying the full balance by the due date will prevent you from accruing interest on your purchases.

6. Managing Credit Responsibly:

- To use a credit card wisely, avoid maxing out your credit limit.

- Aim to pay your balance in full every month to avoid interest charges.

- Monitor your spending and only use the card for necessary purchases.

- Keep track of your due dates and pay on time to maintain a good credit score.

7. Benefits and Rewards:

- Many credit cards offer rewards, such as cashback, travel miles, or discounts on specific purchases.

- Some cards have additional perks, like purchase protection, extended warranties, or travel insurance.

8. Avoiding Debt:

- Credit cards can be a useful financial tool, but they can also lead to debt if not used responsibly.

- Avoid using your credit card to finance a lifestyle beyond your means.

9. Building Credit:

- Responsible use of a credit card can help build your credit history, which can be important for future financial endeavors, like applying for loans or mortgages.

In summary, a credit card can be a convenient and beneficial financial tool when used responsibly. It allows you to make purchases, build credit, and potentially earn rewards. However, it’s essential to manage your credit card wisely to avoid debt and maximize its benefits.

whats is credit card

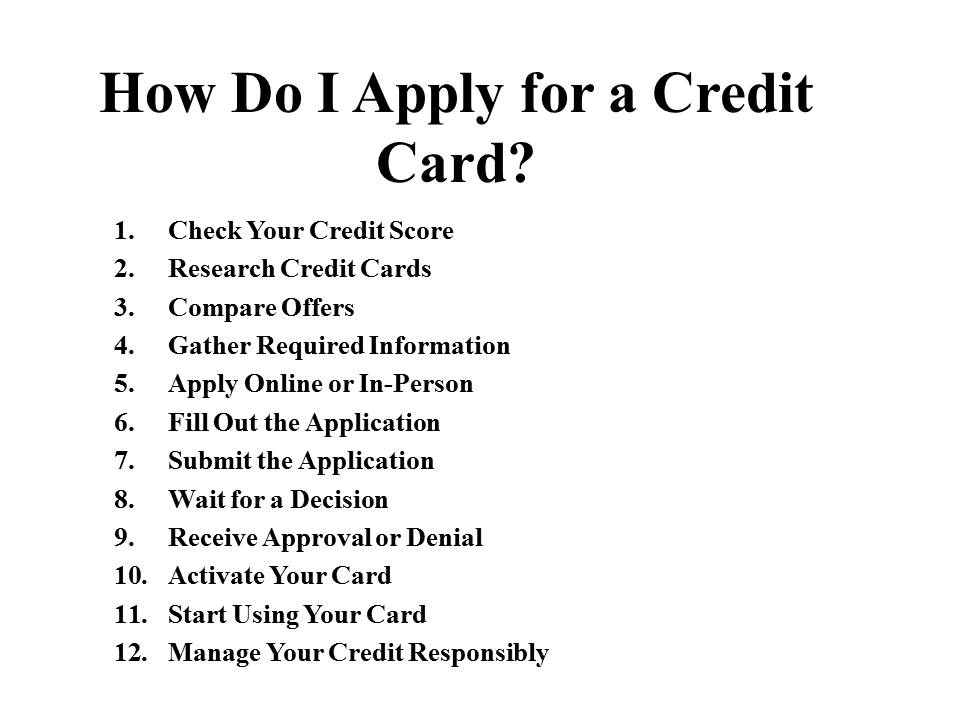

How Do I Apply for a Credit Card?

Applying for a credit card is a relatively straightforward process. Here are the steps to apply for a credit card:

- Check Your Credit Score:

- Before applying, it’s a good idea to check your credit score. Your credit score plays a significant role in the approval process and can affect the terms and credit limit you receive.

- Research Credit Cards:

- Determine what type of credit card you need based on your financial goals and spending habits. Credit cards come in various types, such as rewards cards, low-interest cards, secured cards (for building credit), and more.

- Compare Offers:

- Research and compare credit card offers from different issuers to find the one that best suits your needs. Consider factors like interest rates, annual fees, rewards programs, and credit limits.

- Gather Required Information:

- Before you apply, gather the necessary information, including your Social Security number, income details, employment information, and monthly expenses.

- Apply Online or In-Person:

- You can apply for a credit card online through the issuer’s website or in-person at a bank branch. Most people opt for online applications due to their convenience.

- Fill Out the Application:

- When applying online, you’ll need to complete the application form, providing personal and financial information. Double-check your entries for accuracy.

- Submit the Application:

- After filling out the application, submit it online. Make sure to review the terms and conditions of the credit card offer before finalizing your application.

- Wait for a Decision:

- The credit card issuer will review your application and credit history to make a decision. This process can take anywhere from a few minutes to a few weeks, depending on the issuer.

- Receive Approval or Denial:

- You will receive notice of approval or denial by mail or email. If approved, the issuer will specify the credit limit and terms of your card.

- Activate Your Card:

- Once approved, you’ll typically receive your credit card in the mail. You’ll need to activate it by following the issuer’s instructions, often by calling a phone number or going online.

- Start Using Your Card:

- You can start using your credit card for purchases once it’s activated. Be sure to read and understand the terms and conditions provided by the issuer.

- Manage Your Credit Responsibly:

- After receiving your credit card, use it responsibly by making on-time payments, staying within your credit limit, and avoiding carrying a high balance.

Remember that each credit card application may result in a hard inquiry on your credit report, which can temporarily lower your credit score. Therefore, it’s a good practice to apply for credit cards selectively and only when you believe you meet the eligibility requirements. Additionally, responsible use of credit cards can help you build and maintain a positive credit history.

how to apply for credit card

How Long Does it Take to Get a Credit Card?

The time it takes to get a credit card can vary depending on several factors, including the credit card issuer, the application method, and your specific circumstances. Here’s a general timeline to give you an idea of what to expect:

- Online Applications:

- If you apply for a credit card online, you can often receive a decision within minutes. Some credit card issuers provide instant approval or denial, especially for applicants with good to excellent credit scores.

- In-Person Applications:

- If you apply for a credit card in person at a bank branch or a financial institution, the application process may take a bit longer. You may need to fill out a paper application, and the bank staff will process it. In such cases, it might take a few days to receive a decision.

- Processing Time:

- Once you’re approved for a credit card, it typically takes 7 to 10 business days to receive the physical credit card in the mail. Some issuers may expedite this process and offer expedited shipping for a fee.

- Activation:

- After receiving your credit card, you’ll need to activate it, which usually involves calling a phone number provided by the issuer or going online. Activation is typically a quick process.

- First Statement:

- After activating your card, you can start using it immediately. Your first billing statement will arrive at the end of your card’s billing cycle, which is usually around a month from when you received the card.

- Credit Limit Increase (if requested):

- If you apply for a credit limit increase on your new credit card, it may take some time. The issuer might need to review your payment history and financial situation before granting an increase.

Remember that the timeline can vary based on the issuer’s policies, your credit history, and the specific card you’re applying for. If you’re in a hurry to get a credit card, you may want to apply online for cards with quick approval times. However, it’s essential to research and choose a credit card that aligns with your financial goals and needs rather than solely focusing on the speed of approval. Additionally, always read and understand the terms and conditions of the credit card before applying to ensure it suits your needs.

How are Credit Limits Determined?

Credit limits on credit cards are determined by the credit card issuer, and the process can vary from one issuer to another. The primary factors that influence the credit limit assigned to an individual cardholder include:

- Creditworthiness:

- Your creditworthiness is a crucial factor in determining your credit limit. Lenders assess your creditworthiness based on your credit history and credit score. If you have a strong credit history with a high credit score, you are more likely to be assigned a higher credit limit. Conversely, a poor credit history or a low credit score may result in a lower limit or denial of credit altogether.

- Income:

- Your income plays a role in determining your credit limit. Credit card issuers want to ensure that you have the means to repay your debts. A higher income can lead to a higher credit limit. When you apply for a credit card, you typically need to provide information about your income.

- Employment Status:

- Your employment status and stability can affect the credit limit you’re offered. Lenders may be more comfortable extending higher limits to individuals with stable employment and a consistent source of income.

- Existing Credit Lines:

- If you already have credit cards or loans with other lenders, the total credit you have available (your credit utilization) can influence your credit limit on a new card. High utilization on existing credit accounts may lead to a lower credit limit on a new card.

- Requested Credit Limit:

- Some credit card applications allow you to request a specific credit limit. The issuer may consider your request, but it’s not guaranteed. They will still assess your creditworthiness and other factors.

- Issuer’s Policies:

- Each credit card issuer has its own underwriting criteria and policies for determining credit limits. Some issuers are known for being more generous with credit limits, while others may be more conservative.

- Credit Limit Increases:

- After you’ve had a credit card for some time, you may be eligible for a credit limit increase. Issuers may periodically review your account and offer increases based on your payment history, income, and creditworthiness. You can also request a credit limit increase, but it’s subject to approval.

It’s important to note that credit limits are not fixed and can change over time. Responsible credit card use, on-time payments, and improving your creditworthiness can lead to credit limit increases. Conversely, missed payments or excessive credit card debt can result in limit reductions or account closures.

Remember that your credit limit is not a suggestion of how much you should spend. It’s essential to use credit responsibly, staying well below your credit limit and paying your balance in full or at least making the minimum payment by the due date to avoid fees and interest charges.

Is it Possible to Get Interest Rates Lowered on Credit Cards?

Yes, it is possible to get interest rates lowered on credit cards, but it may not be easy, and it’s not guaranteed. Here are some steps you can take to try to lower the interest rate on your credit card:

- Call Your Credit Card Issuer:

- Start by calling the customer service number on the back of your credit card. Politely explain your situation and ask if they would be willing to lower your interest rate. Sometimes, credit card companies are open to negotiation, especially if you have a good payment history.

- Highlight Your Good Payment History:

- If you’ve been a loyal customer and have consistently made on-time payments, mention this to the representative. A history of responsible credit card use may make the issuer more inclined to work with you.

- Check Your Credit Score:

- Ensure that your credit score is in good shape. A higher credit score can make you more appealing to creditors and improve your chances of negotiating a lower interest rate.

- Shop Around for Balance Transfer Offers:

- Consider transferring your credit card balance to a card with a lower introductory interest rate. Many credit cards offer 0% APR balance transfer promotions for a limited time. Be aware of any balance transfer fees associated with this option.

- Seek a Personal Loan:

- Personal loans often have lower interest rates than credit cards. You could explore the option of taking out a personal loan to pay off high-interest credit card debt and consolidate your debt into a single, lower-interest loan.

- Improve Your Credit Profile:

- Work on improving your overall credit profile. Pay down debt, make on-time payments, and manage your credit responsibly. Over time, these efforts can lead to a better credit score and potentially qualify you for credit cards with lower interest rates.

- Consider a Secured Credit Card:

- If you’re struggling with high-interest rates due to poor credit, you might consider getting a secured credit card to rebuild your credit. These cards typically have lower interest rates than unsecured cards.

- Negotiate with Leverage:

- Sometimes, having leverage can help in negotiations. If you have competing offers from other credit card companies with lower interest rates, you can mention these offers to your current issuer and see if they are willing to match or beat them.

- Be Patient and Persistent:

- If your initial request is declined, don’t give up. Credit card issuers can change their policies, and your financial situation may improve over time. Continue to make on-time payments and periodically check if your issuer is open to reconsidering your interest rate.

Remember that credit card issuers have their own policies and criteria for lowering interest rates, and not all issuers will be willing to do so. Be prepared for the possibility that your request may be declined. Additionally, read any terms and conditions carefully when negotiating lower interest rates to ensure that there are no hidden fees or penalties associated with the change.

What Should You Do if You Want to Dispute a Charge on Your Credit Card Statement?

If you want to dispute a charge on your credit card statement, it’s important to act promptly and follow these steps to resolve the issue:

- Review the Charge:

- Carefully review your credit card statement to ensure that the charge you’re disputing is indeed an error or unauthorized. Sometimes, unfamiliar charges may turn out to be legitimate, such as a purchase you forgot or didn’t recognize immediately.

- Contact the Merchant:

- If you believe the charge is incorrect or unauthorized, the first step is to contact the merchant associated with the charge. You can usually find the merchant’s contact information on your credit card statement or the receipt.

- Explain the issue to the merchant and request a refund or correction. In many cases, the merchant can resolve the issue quickly. Make sure to document your communication with the merchant, including dates and names of representatives you speak with.

- Notify Your Credit Card Issuer:

- If the merchant does not resolve the issue to your satisfaction or if you cannot reach the merchant, contact your credit card issuer promptly. You can usually find a customer service number on the back of your credit card or on your monthly statement.

- Inform the credit card issuer of the disputed charge and explain why you believe it’s incorrect or unauthorized. Be prepared to provide details such as the date of the charge, the amount, and any correspondence with the merchant.

- Many credit card issuers have specific time limits for disputing charges, so it’s essential to act quickly.

- Submit a Written Dispute:

- In some cases, your credit card issuer may require you to submit a written dispute letter. If this is the case, follow their instructions and include all relevant information. Be concise and clear in describing the issue.

- Monitor Your Account:

- While the dispute is being investigated, continue to monitor your credit card account. Pay any undisputed charges by the due date to avoid late fees and interest.

- Your credit card issuer may temporarily remove the disputed amount from your account while they investigate, but you should not rely on this happening.

- Follow Up:

- If your credit card issuer needs more information or documents to process the dispute, provide them promptly. Keep a record of all communication with your issuer.

- Resolution:

- Your credit card issuer will investigate the dispute, and the process may take several weeks. Once the investigation is complete, they will notify you of the resolution. If the charge is found to be incorrect or unauthorized, it will be removed from your account, and you should receive a credit for the disputed amount.

- Know Your Rights:

- Familiarize yourself with your rights under the Fair Credit Billing Act (FCBA). This federal law provides protections to consumers in cases of billing errors and disputes.

- Escalate if Necessary:

- If you are not satisfied with the resolution provided by your credit card issuer, you may have the option to escalate the dispute to a higher level of management within the company or contact regulatory authorities if you believe your rights under the FCBA have been violated.

It’s essential to act quickly when disputing a charge and to keep detailed records of all correspondence and interactions related to the dispute. In most cases, credit card issuers are committed to resolving disputes fairly and promptly to maintain customer satisfaction.

Top of Form